Mega Millions Net Worth: Understanding Your Potential Winnings

Mega Millions is one of America’s most popular lottery games. Millions of people dream of winning the jackpot. But what does “net worth” really mean for lottery winners? This guide breaks down everything you need to know.

The Mega Millions lottery has created countless millionaires. Winners often see their net worth skyrocket overnight. However, the actual amount you take home is different from the advertised jackpot. Understanding this difference is crucial for every player.

What Is Mega Millions Net Worth?

Net worth refers to the actual wealth a lottery winner receives. It’s not just the headline jackpot amount. Several factors reduce the final payout significantly.

When someone wins Mega Millions, they face important choices. The advertised jackpot is an annuity amount. This means it’s paid over 30 years. The cash option is much lower but immediate.

Taxes take a huge bite from lottery winnings. Federal taxes alone consume 24% upfront. State taxes add another layer of reduction. High-earning states can take up to 10% more.

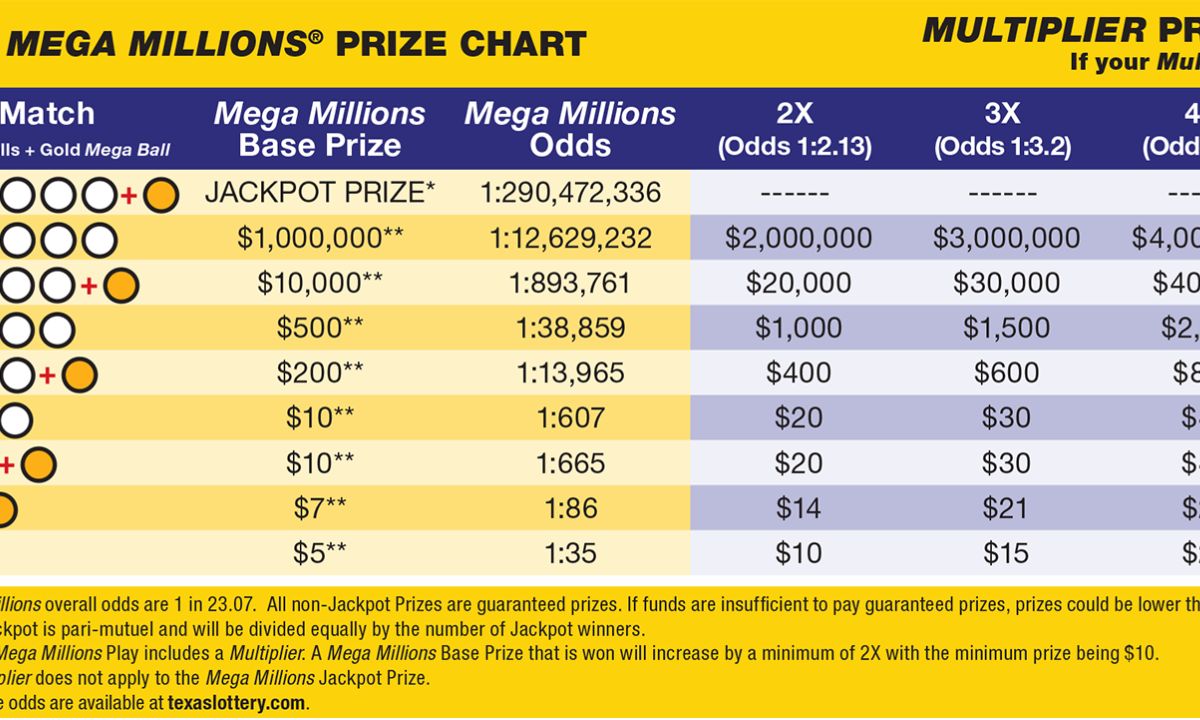

How Mega Millions Jackpots Are Calculated

The jackpot starts at $20 million minimum. It grows with each drawing that has no winner. Ticket sales directly influence jackpot growth. More tickets sold means bigger prizes.

The Multi-State Lottery Association manages Mega Millions. They use complex formulas to determine amounts. Market interest rates affect annuity calculations. Lower rates mean smaller annuity values.

Prize pools come from ticket sales. A portion goes to the jackpot fund. Another portion covers smaller prizes. States also take their share for programs.

Cash Option vs. Annuity: Impact on Net Worth

Winners must choose between two payment options. The annuity pays over 30 years in increasing installments. The cash option provides immediate lump sum payment.

The cash option is roughly 52% of the advertised jackpot. For a $500 million jackpot, cash is about $260 million. This difference shocks many winners. But it’s standard across all lottery games.

Annuity payments increase by 5% annually. This protects against inflation somewhat. The first payment comes immediately. Then annual payments follow for 29 more years.

Most winners choose the cash option. Financial advisors often recommend this route. Immediate access allows better investment opportunities. You can potentially earn more than the annuity rate.

Tax Implications on Mega Millions Winnings

Federal taxes hit lottery winnings hard. The IRS withholds 24% immediately from prizes. But your actual tax rate is likely higher. Lottery winnings are taxed as ordinary income.

For large jackpots, you’ll be in the highest tax bracket. This means a 37% federal tax rate applies. The difference between 24% and 37% is paid at tax time. Many winners are unprepared for this additional burden.

State taxes vary dramatically by location. Seven states have no income tax on lottery winnings. These include Florida, Texas, and Washington. Other states charge between 2.9% and 10.9%.

New York has the highest state lottery tax. Winners there pay 10.9% state tax. Plus New York City adds another 3.876%. Total taxes can exceed 50% of winnings.

Building and Protecting Your New Net Worth

Sudden wealth requires immediate professional help. Financial advisors, lawyers, and accountants are essential. They help you make smart decisions from day one.

Many lottery winners lose everything within years. Poor financial planning destroys fortunes quickly. Lavish spending, bad investments, and family pressure cause problems. Education prevents these common mistakes.

Diversification protects your wealth long-term. Don’t put all your money in one investment. Spread assets across stocks, bonds, and real estate. This reduces risk significantly.

Estate planning becomes critically important. Large estates face substantial taxes without planning. Trusts and other legal structures help. They protect wealth for future generations.

Anonymous claiming protects your privacy where possible. Some states allow winners to remain anonymous. This reduces unwanted attention and requests. Security becomes a real concern with public wins.

Comparison of Mega Millions Jackpot Options

| Factor | Cash Option | Annuity Option |

| Immediate Amount | ~52% of jackpot | First payment only |

| Total Payout | Lower overall | Full advertised amount |

| Payment Schedule | One-time lump sum | 30 annual payments |

| Investment Control | Full immediate control | Limited annual access |

| Tax Impact | Large tax bill at once | Spread over 30 years |

Real-World Examples of Mega Millions Winners

The largest single-ticket Mega Millions winner was in 2018. They won $1.537 billion in South Carolina. The cash value was $877.8 million. After federal taxes, approximately $671.2 million remained.

This winner chose to remain anonymous. South Carolina law allows this protection. They waited several months before claiming. This gave them time to assemble a professional team.

The March 2024 winner in New Jersey won $1.13 billion. They also chose the cash option. The lump sum was approximately $537.5 million. After taxes, roughly $330 million remained.

These examples show the massive tax impact. Winners receive about 35% of advertised jackpots. This includes both cash reduction and taxes. Yet even that amount is life-changing wealth.

Common Mistakes That Reduce Winner Net Worth

Immediate large purchases destroy wealth quickly. Luxury homes, cars, and gifts drain accounts. Winners often buy for family and friends. Generosity is admirable but needs boundaries.

Poor investment choices cause major losses. Risky business ventures often fail completely. Friends and family may pitch investment “opportunities”. Most are poorly conceived or outright scams.

Failing to create a financial plan costs dearly. Without guidance, winners make emotional decisions. Impulse spending becomes normalized quickly. A structured plan prevents this problem.

Smart Strategies for Lottery Winners

Take time before making any decisions. Don’t rush into major purchases immediately. A few months of patience pays off. Use this time to build your team.

Hire fee-only financial advisors who work for you. Avoid commission-based advisors with conflicts of interest. Interview multiple professionals before choosing. Check credentials and references carefully.

Create a comprehensive financial plan immediately. This includes budgets, investments, and goals. Factor in taxes, charitable giving, and family needs. Update the plan regularly as circumstances change.

Establish trusts for asset protection and privacy. These legal structures shield wealth from lawsuits. They also provide tax advantages in some cases. Estate planning attorneys specialize in this area.

Frequently Asked Questions

What is the average net worth of a Mega Millions winner after taxes?

Winners typically receive about 35% of the advertised jackpot after choosing the cash option and paying all taxes, though this varies by state and individual circumstances.

Can you remain anonymous if you win Mega Millions?

Only 18 states allow lottery winners to remain anonymous, including Delaware, Kansas, Maryland, North Dakota, Ohio, South Carolina, and Texas among others.

How long do you have to claim a Mega Millions prize?

Winners have between 90 days to one year to claim prizes depending on the state, with most states allowing 180 days from the drawing date.

What happens to unclaimed Mega Millions prizes?

Unclaimed prizes return to participating states based on their ticket sales percentage, and states use these funds for various purposes including education and lottery operations.

Should you take the lump sum or annuity payment?

Most financial advisors recommend the lump sum because you can invest it for potentially higher returns than the annuity rate, though annuity provides guaranteed income security.

Conclusion

Mega Millions net worth represents life-changing wealth for winners. However, the actual amount differs significantly from headlines. Cash options and taxes reduce jackpots substantially. Smart planning makes the difference between lasting wealth and financial ruin.

Winners need professional guidance from day one. Financial advisors, lawyers, and accountants are essential. They help navigate complex tax situations and investment decisions. Taking time to plan prevents costly mistakes.

![Lumon Definition and Meaning: What It Stands For in Text, Language & Usage [2025]](https://lyricbeet.com/wp-content/uploads/2025/10/Lumon-Definition-and-Meaning-What-It-Stands-For-in-Text-Language-Usage-2025-768x461.jpg)